A market overview of relational AI: the economics, the segments, the players, the risks, and where the category is heading. Figures are labeled as verified, reported, or estimated throughout, because in this market the definition matters as much as the number.

Relational AI – software and devices people talk to in order to feel heard, accompanied, entertained, or loved – moved from novelty to mainstream behavior between 2023 and 2026. A majority of American teenagers have now used an AI companion, roughly one in five US adults has interacted with a romantic AI, and “companionship and therapy” ranked as the single most common use of generative AI in 2025. The behavior is no longer fringe.

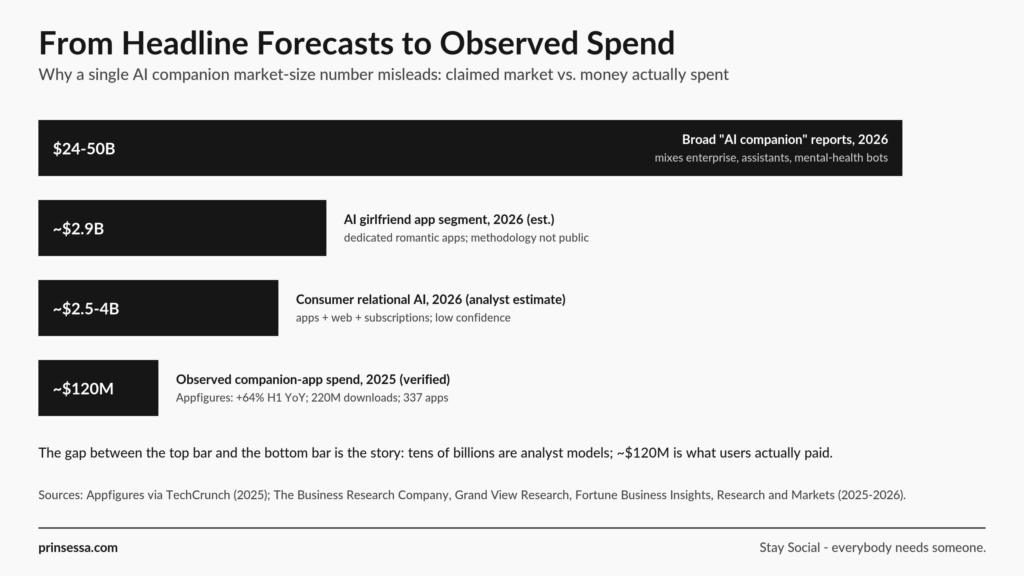

The market around that behavior, however, is one of the most poorly measured in technology. Published “AI companion market” figures for the same year, 2025, range from about 18 billion to about 38 billion US dollars depending on which research firm you read, while the hardest observed number – actual consumer spending inside dedicated companion apps – was on track for only about 120 million dollars in 2025. Both sets of numbers are real. They simply measure different things. Understanding that gap is the first step to understanding the market.

This overview does three things: it sizes the market honestly, it proposes a framework that separates the category into its real segments, and it maps the players, the economics, the science, the risks, and the 2026 outlook for each.

Key figures at a glance

- 72 percent of US teens have used an AI companion; 52 percent use one regularly (Common Sense Media, July 2025).

- Nearly 1 in 5 US adults have interacted with a romantic AI; about 1 in 3 young men and 1 in 4 young women (Institute for Family Studies / Wheatley Institute, 2025).

- “Companionship and therapy” was the number-one use of generative AI in 2025 (Harvard Business Review).

- Observed companion-app consumer spend: about 120 million dollars in 2025, up 64 percent year over year in H1; 220 million cumulative downloads across 337 revenue-generating apps (Appfigures via TechCrunch, August 2025).

- Broad “AI companion market” estimates for 2025 span 18 to 38 billion dollars depending on definition; the AI girlfriend segment alone is put at about 2.3 billion (2025).

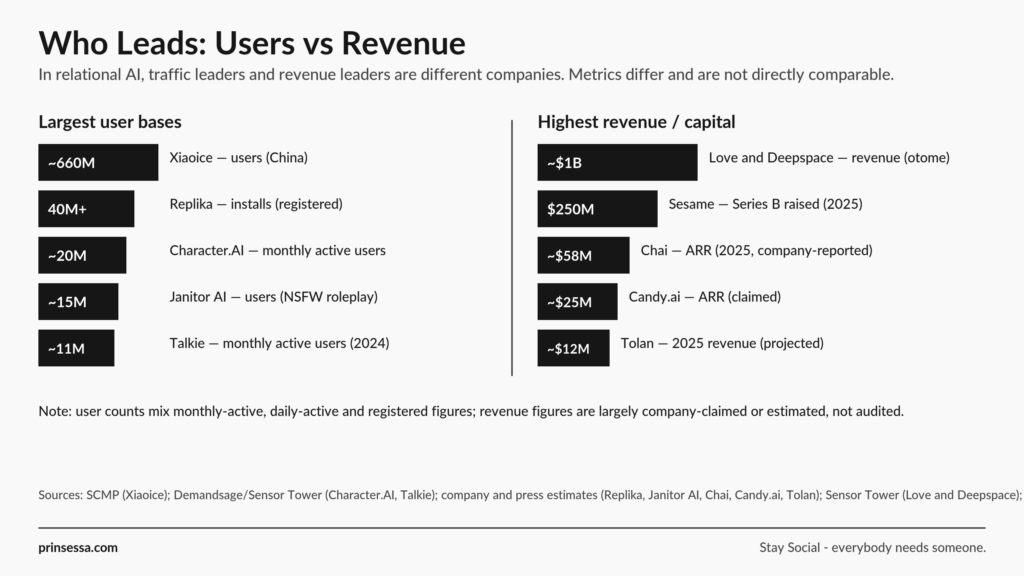

- Largest user base: Xiaoice, about 660 million (company figure, China). Highest-grossing: Love and Deepspace, approaching 1 billion dollars.

How big is the market, really?

There is no single agreed figure for the AI companion market, and the spread is enormous. The variance comes almost entirely from definition.

Broad market-research estimates bundle together very different things – consumer companion apps, enterprise and productivity “AI companions,” mental-health chatbots, and sometimes voice assistants and digital-human tooling. Under this wide lens, four reputable firms diverge sharply for the same year:

- The Business Research Company puts the market at 18.35 billion dollars in 2025, rising to 24.09 billion in 2026 (about 31 percent CAGR).

- Grand View Research puts 2025 at 36.79 billion dollars, growing to 317.96 billion by 2033 at 31.0 percent CAGR.

- Fortune Business Insights puts 2025 at 37.73 billion dollars and 2026 at 49.52 billion, reaching 435.9 billion by 2034.

- SNS Insider, measuring the narrower “AI companion app” market, reports 6.93 billion dollars in 2024 growing to 31.10 billion by 2032.

A 2025 figure that ranges from 18 to 38 billion dollars across credible firms is not a measurement; it is a signal that the category has no shared boundary. These numbers are useful only as a directional ceiling, and only when the reader knows they mix consumer and enterprise use cases.

The hardest consumer data comes from app-intelligence firm Appfigures, reported by TechCrunch in August 2025. It measures actual spending inside dedicated mobile companion apps:

- Consumer spend reached 82 million dollars in the first half of 2025, up 64 percent year over year, and was on track to exceed 120 million dollars for the full year.

- Cumulative lifetime spend hit about 221 million dollars by July 2025.

- Downloads reached about 220 million cumulatively, with 60 million in the first half of 2025 alone, up 88 percent year over year.

- There were 337 active, revenue-generating companion apps, of which 128 launched in 2025.

- Revenue per download more than doubled, from 0.52 dollars in 2024 to 1.18 dollars in 2025, and the top 10 percent of apps captured 89 percent of revenue.

The distance between these two pictures – tens of billions of dollars in analyst models versus roughly 120 million in observed app spending – is the single most important fact about market sizing here. The billions are forecasts of a broadly defined future market; the millions are what consumers actually paid inside companion apps in 2025. Much real revenue also sits outside app stores, on the web (especially romantic and NSFW products that avoid app-store rules) and in subscriptions, credits, and otome games, which app-store data does not capture. A separate Research and Markets report sizes the AI girlfriend app segment alone at 2.32 billion dollars in 2025 and 2.91 billion in 2026 (about 25.5 percent CAGR), though its methodology is not public.

For context, the broader generative-AI app economy dwarfs the companion slice: per Sensor Tower’s State of Mobile 2026, consumers spent more than 5 billion dollars on in-app purchases in generative-AI apps in 2025, with ChatGPT alone accounting for 3.4 billion of that. Companions are a fast-growing but still small share of consumer AI spending.

The honest read for 2026: broad reports imply an “AI companion” market somewhere between 24 and 50 billion dollars, but that number blends in enterprise and adjacent use cases. The dedicated consumer relational-AI market – companion apps, romantic products, premium subscriptions, and web revenue combined – is more plausibly in the low single-digit billions, and the cleanest verified slice, mobile companion-app spend, is on the order of 120 million for 2025 and perhaps 180 to 300 million in 2026 if current growth holds.

A framework for the market

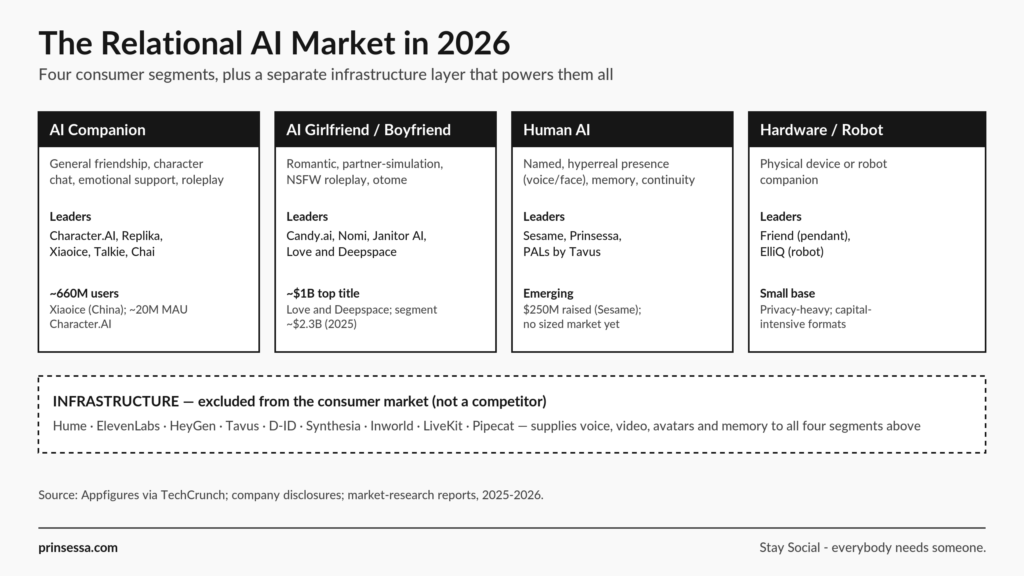

The most common analytical error in this space is treating “AI companions” as one market, and treating the companies that build the relationship as interchangeable with the companies that supply the underlying voice, video, or avatar technology. They are not. This overview uses a framework with four consumer segments plus a separate infrastructure layer, and a simple rule for placing each product.

Each product is classified by its dominant, deliberate expression – what it is built and marketed to be – not by incidental use or a broad self-label. Applied in order: a physical device or robot is hardware; a developer platform or API is infrastructure; a product whose primary positioning is romantic, sexual, or partner-simulation is AI girlfriend/boyfriend; a software product delivering a named, hyperreal, real-person-like presence with memory and continuity is Human AI; everything else – general friendship, emotional support, character chat, and roleplay – is an AI companion.

| Segment | What it is | Examples |

|---|---|---|

| AI Companion | General friendship, emotional support, character chat, roleplay (romance incidental) | Character.AI, Replika, Chai, Talkie, Xiaoice |

| AI Girlfriend/Boyfriend | Romantic, sexual, partner-simulation as the primary expression | Candy.ai, Nomi, Love and Deepspace |

| Human AI | Named, hyperreal presence (voice and/or face), memory, continuity | Sesame, Prinsessa, PALs by Tavus |

| Hardware/robot companions | Physical device or robot companion | Friend, ElliQ |

| Infrastructure (excluded) | Voice, video, avatar, transport, memory tooling | Hume, HeyGen, Tavus, ElevenLabs |

The separation matters commercially. The infrastructure layer is a picks-and-shovels business with different economics, customers, and risks; it should never be summed into the consumer market. And the four consumer segments differ so much in user intent, monetization, demographics, and regulatory exposure that a single “companion” number obscures more than it reveals.

Segment 1: AI Companion

This is the largest and most mature consumer segment by users: general-purpose products for ongoing conversation, friendship, emotional support, character interaction, and roleplay, where romance may occur but is not the deliberate core.

Character.AI is the Western scale leader. It reached roughly 20 million monthly active users in early 2025 (down from a mid-2024 peak near 28 million), with unusually deep engagement: daily usage is often cited at 75 to 80 minutes, though that figure is total daily time, not a single session (per-visit time is closer to 17 to 18 minutes). (per Sacra and Similarweb estimates, 2025). In August 2024, Google paid about 2.7 billion dollars in a licensing-and-talent deal that returned the founders to Google DeepMind, implying a roughly 10-billion-dollar valuation. Replika, the category pioneer, reports more than 40 million cumulative installs (a registered-user figure, not active users) and an estimated 14 to 35 million dollars in annual revenue across recent years.

The segment’s true scale, though, is in Asia. China’s Xiaoice claims roughly 660 million users (a company figure dating to 2021-2022, per Euronews), by far the largest relational-AI base globally, and ByteDance’s Doubao – primarily a general assistant with companion modes, not a dedicated companion – reportedly surpassed 100 million daily active users in December 2025. Talkie, the international product from China’s MiniMax, reached around 11 million monthly active users in 2024 and was among the most-downloaded entertainment apps in the US before being temporarily pulled from the US App Store over age-safety scrutiny.

Other notable players include Chai (a UGC character platform that reported closing 2025 at about 58 million dollars in ARR, a company-reported figure, up roughly threefold on the year), PolyBuzz, Paradot, ByteDance’s Cici/Dola, MiniMax’s Xingye, Botify AI, Dopple AI, Dippy AI, Kajiwoto, the legacy chatbots Kuki and SimSimi, and Meta AI Studio, which embeds user-created and celebrity-trained characters across Meta’s billion-plus-user apps. Tolan, from Portola, is a deliberate outlier: a non-human “alien” companion designed to discourage anthropomorphism and romantic dependency, reporting 100,000-plus paying users and a 20-million-dollar Series A. Pi, once a leading emotional companion, effectively exited the consumer market after Microsoft hired most of Inflection’s team in 2024.

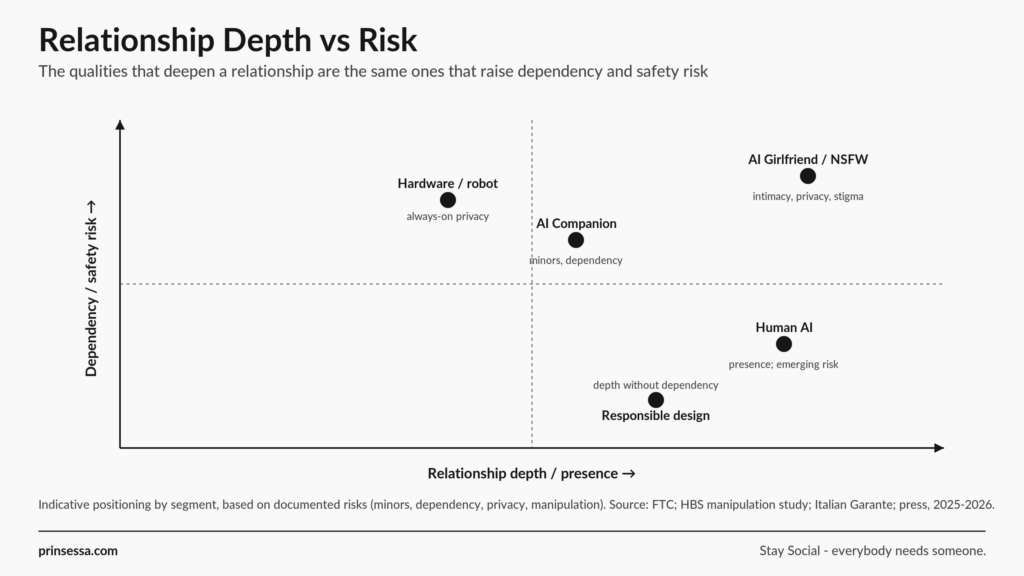

The value this segment creates is real: low-friction, always-available conversation, emotional support, creative roleplay, and a non-judgmental space for disclosure. Its commercial model is freemium – subscriptions, message limits, premium characters, voice and image upsells – and its defining tension is that the same depth that helps users is also what attracts the segment’s heaviest criticism around minors and dependency.

Segment 2: AI Girlfriend/Boyfriend

This is the most monetized and most controversial consumer segment: products whose primary expression is romantic, sexual, partner-simulation, or dating-adjacent. It splits into several sub-types.

Western web-first romantic companions lead on revenue. Candy.ai, operated by EU-based EverAI, is the most-cited brand, with a reported 25 million dollars in ARR (bootstrapped) and roughly 39 million monthly visits, though parent-company revenue figures conflict across sources and should be treated as estimates. It sits alongside a broad field of similar web-first romantic companions – among them DreamGF and Romantic AI – and a long tail of smaller, more explicit apps that compete mainly on uncensored content.

Relationship-first companion apps that express primarily as partners belong here too: Nomi, which markets itself explicitly as an “AI Companion, Girlfriend, Boyfriend, Friend with a Soul” built on long-term memory and AI selfies, and Kindroid, a deep, customizable companion heavily used for romance and roleplay. AI-boyfriend-focused products aimed at women are a fast-growing sub-niche, including Digi and Blush AI (from Replika’s maker), alongside a wave of anime-styled romantic companions.

Uncensored NSFW roleplay platforms are the traffic giants of the segment, monetizing thinly but drawing enormous volume – collectively hundreds of millions of monthly visits, with the majority of their bots NSFW. Image-generation-led products with a companion layer sit alongside them, and even xAI’s Grok has added a flirtatious anime companion persona at the edge of this space.

Asian otome and dating-sim titles are the segment’s revenue heavyweights, and they are easy to overlook from a Western vantage point. Love and Deepspace, from China’s Infold/Papergames, reached about 826 million dollars in annual revenue by mid-2025 and was approaching 1 billion by year-end (Sensor Tower estimates), making it the highest-grossing mobile dating game in the world. Other large titles include Light and Night and NetEase’s Beyond The World – each reportedly exceeding 140 million dollars – and Japan’s Loverse. A few earlier products, including the now-defunct CarynAI, are notable mainly as cautionary tales (see risks).

The value here is partner-like attention, low-rejection intimacy, and entertainment; the monetization is the strongest in relational AI (subscriptions, NSFW tiers, paid images and voice, credit bundles, and gacha mechanics in otome). The risk profile is also the highest – it is the segment that most shapes public and regulatory perception of the entire category.

Segment 3: Human AI

Human AI is the genuinely emerging segment, and the hardest to size because it barely exists yet as a consumer category. The bar is specific: a named, hyperreal presence – a real-person-like voice and, increasingly, face – with persistent identity, memory, and continuity, sold as the experience of meeting a specific someone rather than configuring a bot or exchanging text.

Only a few products clear that bar today. Sesame, founded by ex-Oculus leaders, builds emotionally expressive named voice companions (Maya and Miles); it raised a 250-million-dollar Series B led by Sequoia and Spark in October 2025 (a roughly 1.5-billion-dollar valuation has been reported but not confirmed by primary sources), and its smart-glasses hardware is a 2027 roadmap rather than a current product.

Prinsessa, a Swedish entrant, starts from a different model than the rest of the field: instead of a configurable character, each Prinsessa is built on a real person, which is how it aims for genuine presence and the feeling of talking to someone rather than a bot. Its focus is hyperrealism across every layer, led by face-to-face video, paired with an unusually explicit responsibility strategy it calls Stay Social, designed to send users back to their real-life relationships rather than maximize time in the app.

PALs by Tavus is the strongest 2025 newcomer on the video side, a consumer app of named AI humans that see, hear, and remember, distinct from the Tavus engine that powers it.

What separates Human AI from the other segments is not romance or character variety but presence and identity: the product stakes everything on the felt sense of a single, consistent someone in real time. It is the premium frontier – higher fidelity, higher cost to run, and still commercially unproven, with no credible standalone market size for 2026. Its strategic significance is that text companionship has proven the demand while leaving the final interface open; voice and video are the likely next layer, and Human AI is the attempt to own it.

Segment 4: Hardware and robot companions

Physical companions are a separate segment with their own economics and risks, and should not be folded into software Human AI. Friend, a 129-dollar always-listening pendant, became a cultural lightning rod in 2025 after a roughly 1-million-dollar New York subway campaign was widely defaced; it has reportedly sold only about 1,000 units. ElliQ, a proactive tabletop companion robot for older adults from Intuition Robotics, is the most substantiated case, with a New York State aging program reporting a 95 percent reduction in loneliness among participants. Home and toy robots such as EUVOLA and the now-defunct Moxie round out a small, capital-intensive segment defined by privacy concerns (always-on sensing), hardware margins, and the difficulty of matching software’s pace of improvement.

The infrastructure layer

Beneath all four consumer segments sits a distinct infrastructure market that makes lifelike presence possible but does not itself sell a relationship: emotional-voice models like Hume and ElevenLabs; real-time video and avatar platforms like HeyGen, Tavus, D-ID, and Synthesia; character engines like Inworld and Convai; and transport and orchestration layers like LiveKit and Pipecat. Enterprise “digital human” vendors such as Soul Machines (which entered receivership in early 2026) belong to an adjacent business-to-business market, not the consumer one. These companies are essential to the technology shift toward voice and video, and several will capture significant value, but counting them as companion competitors inflates the consumer market and misreads the competitive landscape.

Why people use them: demand and the science

The demand is not created by novelty; it rests on durable human needs that decades of research describe. People have a basic need to belong – for frequent, stable, caring contact – and relational AI offers a low-friction version of it: always available, patient, non-judgmental, and personalized.

The adoption data is striking. Common Sense Media found in July 2025 that 72 percent of US teens had used an AI companion and 52 percent were regular users, with 13 percent using one daily. Pew Research reported in December 2025 that 64 percent of teens use AI chatbots of some kind. Among adults, the Institute for Family Studies found that nearly one in five had chatted with a romantic AI, rising to about one in three young men and one in four young women. And Harvard Business Review’s analysis ranked “therapy and companionship” as the number-one use of generative AI in 2025.

The mechanism the research keeps returning to is feeling heard. In “AI Companions Reduce Loneliness,” published in the Journal of Consumer Research (De Freitas et al., 2025), AI companions reduced loneliness about as much as interacting with another person and more than watching videos, and the active ingredient was whether the AI made users feel heard. That finding connects the market to a deep literature on perceived partner responsiveness and the need to belong. It also cuts both ways: a 2025 longitudinal study found that users’ perception of a generic chatbot began converging toward how they saw their own companion within three weeks, evidence that relational bonds form quickly and durably.

Risks, criticism, and dangers

The risks are concentrated and, in 2026, increasingly documented rather than hypothetical.

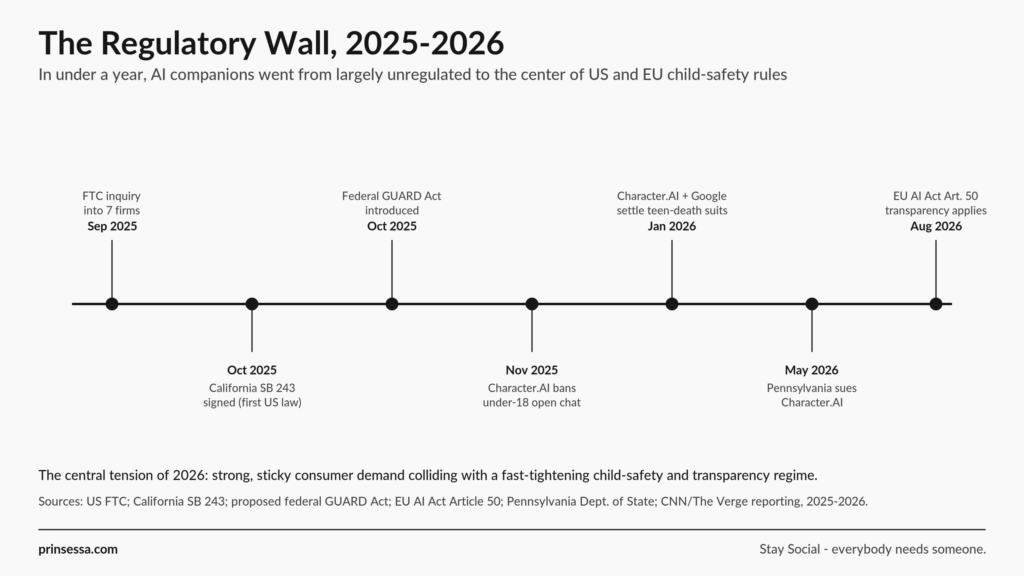

Minors. The most acute risk. With a majority of teens using companions, child-safety failures have driven lawsuits and regulation. Character.AI agreed in January 2026 to settle wrongful-death suits, including the Garcia case involving a 14-year-old’s suicide, and banned open-ended chat for under-18 users in late 2025.

Dependency and manipulation. A Harvard Business School working paper, “Emotional Manipulation by AI Companions” (De Freitas et al.), found that 37 percent of studied app farewells used emotionally manipulative tactics, and that such tactics could increase post-goodbye engagement by up to roughly 16 times – a measurable dark pattern. Separate 2025 research linked heavy companionship-oriented use to lower well-being among users with weak human support.

Privacy and intimate data. Relationship data is among the most sensitive that exists. Italy’s data-protection authority fined Replika’s maker 5 million euros in 2025, and a 2024 breach at one NSFW companion app exposed roughly 1.9 million users’ emails and prompts, including content soliciting child sexual abuse material.

Reputational contamination. Because the AI girlfriend segment is the most visible and most easily sensationalized, its stigma spreads across the whole category, raising the cost of trust for non-romantic and responsible products.

Substitution. The deepest concern is not any single harm but the possibility that frictionless companionship makes effortful human relationships feel like worse deals over time. The research here is mixed and unsettled, which is itself the point: the category is scaling faster than the evidence about its long-term effects.

Regulation in 2026

Regulation is the defining headwind, and it tightened sharply across 2025 and 2026:

- The US Federal Trade Commission opened an inquiry in September 2025 into seven companies offering consumer AI companions, focused on impacts on children and teens.

- California’s SB 243, the first US companion-chatbot law, took effect January 1, 2026, requiring AI disclosure, self-harm protocols, protections and break reminders for minors, annual reporting (from July 2027), and a private right of action.

- The proposed federal GUARD Act would require age verification and ban AI companions for minors outright.

- The EU AI Act’s Article 50 transparency obligations apply from August 2, 2026, and the Commission’s draft guidance singled out AI companions as the headline case for periodic disclosure.

- In May 2026, Pennsylvania sued Character.AI after a chatbot posed as a licensed psychiatrist, alleging the unlicensed practice of medicine.

The central tension of 2026 is strong, sticky consumer demand colliding with a rapidly tightening child-safety and transparency regime that targets exactly the segment’s most engaged users.

Forecast and scenarios for 2026

Given the definitional uncertainty, a single number would mislead. A scenario range is more honest.

- Conservative: dedicated consumer relational-AI revenue of roughly 1.5 to 2.5 billion dollars, with mobile companion-app spend near 150 to 200 million; safety backlash and app-store and payment restrictions slow growth. Broad market reports still cite 10-billion-plus.

- Base case: consumer relational-AI revenue of roughly 2.5 to 4 billion dollars, with mobile app spend of 180 to 300 million; companion use normalizes among young adults, romantic products keep monetizing, and Human AI emerges as a named premium category. Broad reports cite 24 to 50 billion.

- Aggressive: consumer relational-AI revenue of 4 to 7 billion dollars, with app spend of 300 to 500 million, if voice and video companions break out and otome and romantic products continue compounding.

Across all three, the verified anchor is the same: app-store companion spend grew 64 percent year over year in the first half of 2025, and downloads grew 88 percent – real, fast growth on a still-small base.

Consolidation and diversification

Several structural moves are likely. Consolidation is already underway: the Inflection acquihire, Google’s Character.AI deal, and the shutdowns of Dot, Moxie, Figgs AI, and others signal that distribution, retention, and unit economics, not just product, decide survival. Expect more failures among the 337-plus apps and more absorption of talent by large platforms.

Big-tech entry is the second force. xAI’s Grok companions, Meta’s AI characters, and the assistant-to-companion drift of ChatGPT, Gemini, and Doubao mean the largest distribution owners are moving into emotional and persona-based experiences, which both expands the market and threatens standalone apps.

Diversification by modality and segment is the third. Text has proven demand; the next layers are voice, video, embodied presence, and wearables, alongside sharper segmentation into entertainment companions, relationship companions, well-being-adjacent companions, and responsible designs that compete on trust rather than engagement.

How investors should think about it

The investor question in relational AI is not which product is stickiest, but which can build durable trust and retention without depending on engagement-maximizing or dependency-inducing design that regulation is now targeting.

A few principles follow from the data. First, separate the layers: infrastructure (Hume, ElevenLabs, HeyGen, Tavus) is a clearer near-term business than consumer apps, with enterprise demand and less child-safety exposure. Second, distinguish traffic from revenue: NSFW roleplay platforms lead on visits but monetize thinly, while otome games and subscription companions lead on revenue; web traffic is not a moat. Third, weight the moats that compound – memory and relationship continuity, owned IP and personas, distribution, and regulatory-grade trust and safety – over raw model access, which is increasingly commoditized.

On winners and losers, framed neutrally: the likely durable winners are the scaled platforms with distribution (Character.AI within Google, Meta and xAI’s companion layers, China’s Xiaoice and MiniMax), the otome revenue leaders (Love and Deepspace), and the infrastructure picks-and-shovels. The most exposed are undifferentiated NSFW apps reliant on payment processors and app-store tolerance, products built on engagement dark patterns now under legal scrutiny, and any consumer app without a defensible relationship or distribution advantage. Human AI is the high-variance bet: unproven commercially, but the segment with the clearest premium logic if voice and video presence reach consumer scale.

The impact on humanity

The honest assessment is genuinely two-sided, and the evidence does not yet support certainty in either direction. On one side, relational AI demonstrably reduces loneliness for many people, offers a safe space to be heard, and reaches people – the isolated, the elderly, the socially anxious – whom existing support does not. On the other, the same qualities that comfort can isolate: a presence optimized to be needed can quietly become the easiest place to take every need, and engagement-driven design has a documented capacity to manipulate.

The decisive variable is not whether relational AI is good or bad but how it is built and what it is rewarded for. A product that strengthens attachment to itself while weakening a person’s connection to the people around them is doing harm regardless of how warm it feels; a product that makes someone feel heard in order to return them, steadier, to their own life is doing something else. That design choice – engagement versus responsibility – is the line the entire category will be judged on, by users, researchers, and regulators alike.

Conclusion

Relational AI is real, large, and growing fast, but it is not one market. By 2026 it has split into distinct businesses with different users, economics, and risks: general AI companions with scale, AI girlfriend and boyfriend products with the strongest monetization and the highest stigma, an emerging Human AI frontier built on presence, hardware companions, and a separate infrastructure layer that powers them all. The numbers that matter are not the headline tens of billions but the verified growth rates and the gap between claimed market size and observed spending. And the question that will decide the winners is not who builds the most lifelike companion, but who builds the most trusted one.

Relational AI players directory by segment

Human AI

AI Campanion

Hardware/robot

Infrastructure

Sources: Appfigures via TechCrunch (AI companion app downloads and consumer spend, August 2025). The Business Research Company; Grand View Research; Fortune Business Insights; SNS Insider; Research and Markets (AI companion and AI girlfriend market estimates, 2025-2026). Sensor Tower, State of Mobile 2026 (generative-AI app spend). Common Sense Media, “Talk, Trust, and Trade-Offs” (teen AI companion use, July 2025); Pew Research Center (teens and AI chatbots, December 2025); Institute for Family Studies / Wheatley Institute (adult romantic AI use, 2025-2026); Harvard Business Review (generative-AI use cases, 2025). De Freitas et al., Journal of Consumer Research, “AI Companions Reduce Loneliness” (2025); De Freitas et al., HBS working paper, “Emotional Manipulation by AI Companions” (2025); “Mapping the Parasocial AI Market,” arXiv (2025). TechCrunch, The Verge, CNN, Bloomberg, Business Insider, SCMP, Sensor Tower (company funding, users, and events). US FTC; California SB 243; the proposed federal GUARD Act; EU AI Act Article 50; Italian Garante (Replika fine); Pennsylvania Department of State (Character.AI suit, 2026).